(All amounts in US$ unless otherwise indicated)

VANCOUVER, British Columbia – Capstone Copper Corp. («Capstone» or the «Company») (TSX:CS) (ASX:CSC) today announced the results of an updated feasibility study («FS») for its 100%-owned, fully-permitted Santo Domingo copper-iron-gold project («Santo Domingo» or the «Project») in Region III, Chile, located 35 kilometres northeast of its 70%-owned Mantoverde mine.

«The release of the updated feasibility study for our Santo Domingo Project marks a major step towards the creation of a world-class district in the Atacama region of Chile. We have optimized the mine plan, updated the capital and operating cost estimates, and incorporated all experience gained throughout the engineering and construction of our nearby Mantoverde Development Project», John MacKenzie, Capstone’s Chief Executive Officer, commented. «The 2024 feasibility study significantly enhances the mine’s economics backed by low capital intensity and first quartile costs. A construction decision and the integration of Santo Domingo represents the next phase of our transformational growth as we become a leading long-life and low-cost producer of critical metals essential for the world’s decarbonization efforts. We now intend to progress with the assessment of the optimal financing structure for the project, which may include bringing in a minority partner at the project level. In parallel we will also continue to advance the detailed engineering on the project. Our team is committed to pursuing the highest standards in safety and environmental management as well as continued engagement with all stakeholders as we progress our growth plans.»

2024 SANTO DOMINGO FEASIBILITY STUDY SUMMARY

- The 2024 FS outlines a robust copper-iron-gold project with an after-tax net present value at an 8% discount rate («NPV8%«) of $1.7 billion and an after-tax internal rate of return («IRR») of 24.1%

- Over the first seven years of the mine plan, production is expected to average 106,000 tonnes of copper and 3.7 million tonnes of iron concentrate at first quartile cash costs of $0.28 per payable pound of copper produced

- Over the Project’s 19-year mine life, production is expected to average 68,000 tonnes of copper and 3.6 million tonnes of iron concentrate at first quartile cash costs of $0.33 per payable pound of copper produced

- Total initial capital cost of $2.3 billion drives a capital intensity of approximately $21,900 per tonne of annual copper equivalent production over the life of mine

- A 19-year mine life is supported by a higher Mineral Reserve1 estimate of 436 million tonnes at a copper grade of 0.33%, iron ore grade of 26.5%, and a gold grade of 0.05 grams per tonne

- Mineral Reserve tonnes have increased by 11% while contained copper has increased by 23% since the 2020 Feasibility Study

- Total Measured and Indicated («M&I») Mineral Resources of 547 million tonnes at a copper grade of 0.31% and a gold grade of 0.04 grams per tonne, including 506 million tonnes with an iron grade of 25.8%

- M&I Resource tonnes increased by 2% while contained copper in M&I Resources increased by 6% since the 2020 Feasibility Study

- The Company plans to progress several value enhancement initiatives within the Mantoverde-Santo Domingo («MV-SD») district that are noted in the Opportunities section but not yet incorporated into the base case 2024 FS, including:

- The processing of Santo Domingo’s oxide material using Mantoverde’s excess SX-EW capacity

- The recovery of cobalt and additional copper from a pyrite concentrate

- Ongoing exploration of the MV-SD district, including the recently acquired Sierra Norte deposit

For a virtual tour of Santo Domingo and the MV-SD district, please visit: https://youtu.be/n-FyVJ9t2JE

1 Comprised of 131 million tonnes in the Proven category and 305 million tonnes in the Probable category. Please refer to the detailed breakdown of the Santo Domingo Mineral Reserve estimate below.

SUMMARY OF RESULTS

The 2024 FS reflects the results of the Company’s further technical and optimization work at Santo Domingo. A summary of key financial, production, cost, and operating details from the 2024 FS can be found below, in addition to a comparison to the previous Feasibility Study published in 2020. For further details, please refer to Exhibit 1 at the end of this news release.

|

|

2024 Feasibility Study |

2020 Feasibility Study |

|

Life of Mine («LOM») (years) |

19 |

18 |

|

Initial capital cost (US$ billions) |

$2.3 |

$1.5 |

|

After-tax NPV(8%) (US$ billions) |

$1.7 |

$1.3 |

|

After-tax IRR (%) |

24.1% |

21.8% |

|

After-tax Payback period (years) |

3.0 |

2.8 |

|

Average Annual First Seven Years of Production |

|

|

|

Copper («Cu») production2 (thousand tonnes) |

106 |

103 |

|

Iron concentrate production («Fe») (million tonnes) |

3.7 |

3.3 |

|

Gold production («Au») (thousand ounces) |

35 |

30 |

|

C1 cash costs per pound of payable copper produced (by-product basis) |

$0.283 |

$0.612 |

|

C1 cash costs per pound of payable copper equivalent produced (co-product basis) |

$1.274 |

$1.163 |

|

Average Annual for LOM |

|

|

|

Copper production (thousand tonnes)5 |

68 |

62 |

|

Iron concentrate production (million tonnes) |

3.6 |

4.2 |

|

Gold production (thousand ounces) |

22 |

17 |

|

C1 cash costs per pound of payable copper produced (by-product basis) |

$0.332 |

$0.022 |

|

C1 cash costs per pound of payable copper equivalent produced (co-product basis) |

$1.593 |

$1.403 |

2 Contained production includes recovery loss.

3 C1 cash costs are net of magnetite iron and gold by-product credits and selling costs. These are Non-GAAP performance measures; please see «Non-GAAP and Other Performance Measures» at the end of this news release.

4 C1 cash costs on a co-product basis consist of mining costs, processing costs, mine-level G&A, gold revenue credit, and refining charges over payable copper equivalent pounds (copper plus magnetite). These are Non-GAAP performance measures; please see «Non-GAAP and Other Performance Measures» at the end of this news release.

5 After recovery loss.

| First Seven Years Operating Statistics Summary |

2024 Feasibility Study |

2020 Feasibility Study |

|

Total tonnes milled (million tonnes) |

172.6 |

162.1 |

|

Strip ratio (waste to ore) |

2.3:1 |

3.4:1 |

|

Head Grade |

|

|

|

Copper (% Cu) |

0.48 |

0.48 |

|

Iron (% Fe) |

29.0 |

29.3 |

|

Gold (g/t Au) |

0.07 |

0.06 |

|

Recovery |

|

|

|

Copper5 |

90.3% |

93.8% |

|

Iron mass |

15.1% |

14.1% |

|

Gold |

67.8% |

63.2% |

|

Life of Mine Operating Statistics Summary |

2024 Feasibility Study |

2020 Feasibility Study |

|

Total tonnes milled (million tonnes) |

436.1 |

392.3 |

|

Strip ratio (waste to ore) |

2.5:1 |

3.3:1 |

|

Head Grade |

|

|

|

Copper (% Cu) |

0.33 |

0.30 |

|

Iron (% Fe) |

26.5 |

28.2 |

|

Gold (g/t Au) |

0.05 |

0.04 |

|

Recovery |

|

|

|

Copper6 |

90.1% |

93.4% |

|

Iron mass |

15.7% |

19.1% |

|

Gold |

64.7% |

60.1% |

|

Commodity Price Assumptions |

|

|

|

Copper (per pound) |

$4.10 |

$3.00 |

|

P65 Index CFR China iron ore (per tonne) 7 |

$110 |

$93 |

|

Gold (per ounce) |

$1,800 |

$1,280 |

Project Valuation Metrics – Price Sensitivities

|

|

NPV (after-tax, 8% discount) (US$ billions) |

IRR (after-tax) (%) |

Payback period (after-tax) (years) |

|

Santo Domingo Cu-Fe-Au Project |

|||

|

Base Case pricing +10% |

$2.10 |

27.2% |

2.8 |

|

Base Case pricing |

$1.72 |

24.1% |

3.0 |

|

Base Case pricing -10% |

$1.34 |

20.8% |

3.4 |

6 Copper recovery is for the copper concentrator only.

7 The 2024 FS includes three iron ore magnetite products, a 62% Fe magnetite, a 65% Fe magnetite, and a 67% Fe magnetite. For more details regarding the pricing breakdown, please see section «Commodity Pricing – Iron Ore» and Exhibit 1.

Cashel Meagher, President and COO, commented, «The mine plan presented today at Santo Domingo represents the next major step for Capstone in the evolution of the world-class Mantoverde-Santo Domingo district. Having recently completed construction at our Mantoverde Development Project, we have an experienced mine-build team which today is rare in our industry. The feasibility study for Santo Domingo outlines an actionable investment opportunity with an attractive rate of return and a short payback period. Over time, we plan to further augment these base case numbers with additional opportunities, including unlocking cobalt production in the district, processing Santo Domingo’s oxides at Mantoverde, and continuing to explore the district to improve our understanding of the longer-term potential. The plan presented today sets the stage for two major processing centers in our world class Mantoverde-Santo Domingo district.»

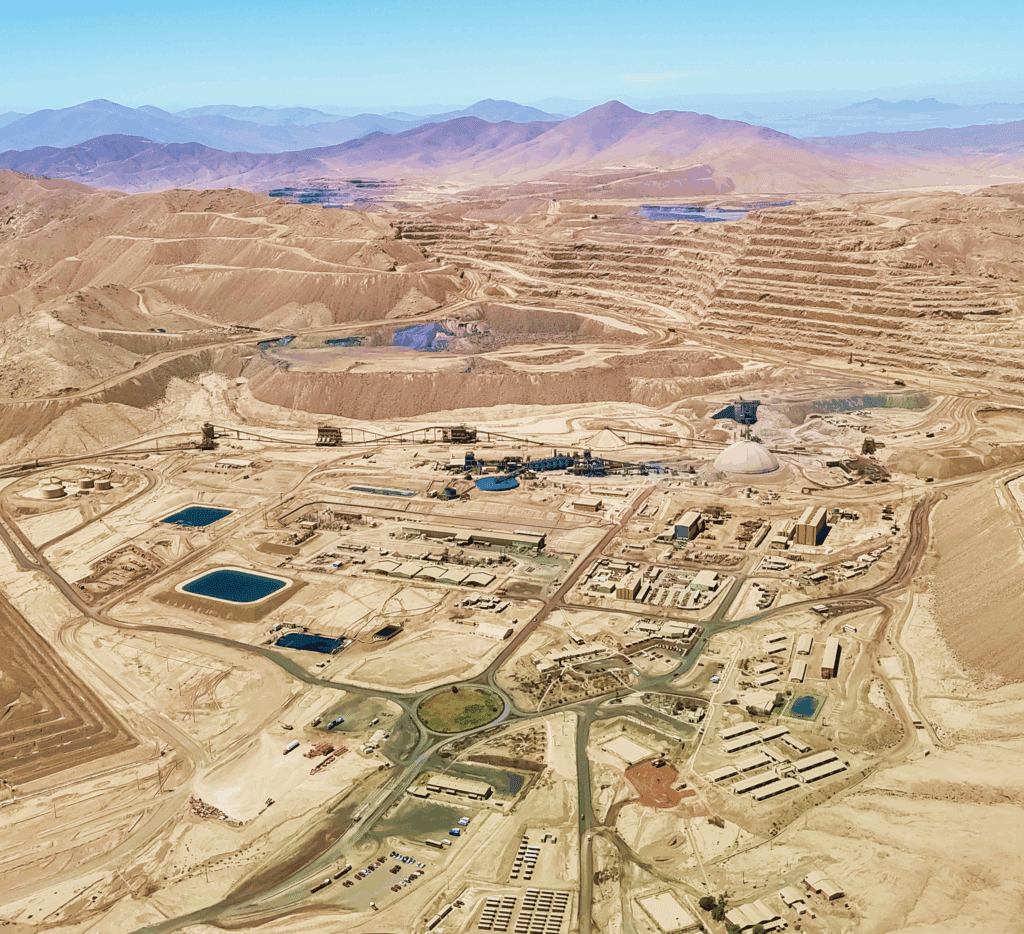

SANTO DOMINGO PROJECT DESIGN

The updated Santo Domingo 2024 feasibility study was prepared by Ausenco Chile Limitada, part of Ausenco, a multinational engineering, procurement, construction management, and operations service provider with broad international experience in the design and construction of concentrator projects of this scale. Ausenco was specifically responsible for the construction of Capstone’s nearby Mantoverde Development Project, which was completed under a lump-sum turn-key engineering, procurement, and construction («EPC») contract.

The Santo Domingo project includes development of two open pit mines using conventional drilling, blasting, and loading with electric and hydraulic shovels. The project includes a copper-iron concentrator designed to process a maximum of 72,000 tonnes per day using Autogenous Grinding («AG») milling, with conventional rougher cell flotation, regrinding and classification, with Jameson Cells used in the cleaner, cleaner scalper, cleaner scavenger, and re-cleaner stages. Magnetite iron will be recovered from the copper rougher tailings using Low Intensity Magnetic Separation. The planned infrastructure includes a tailings storage facility («TSF»); an iron magnetite concentrate pipeline and a third party operated desalination plant and desalinated water supply pipeline; a port-located magnetite iron concentrate filter plant and stockpile; a port-located copper concentrate storage building; ship loading facilities; a high voltage transmission line; and on-site and off-site infrastructure and support facilities.

The Project is located 35 kilometres northeast of our Mantoverde copper-gold mine, 50 kilometres southwest of Codelco’s El Salvador copper mine, and 130 kilometres north-northeast of Copiapó, near the town of Diego de Almagro, in Region III, Chile. The elevation at the site is approximately 1,000 metres above sea level («masl») with relatively gentle topographic relief. Access to the property is one kilometre off the paved highway C-17 from Diego de Almagro to Copiapó. The magnetite filter plant and stockpile, the copper storage building, the desalination plant and other port infrastructure will be located in Punta Roca Blanca, 43 kilometres north of Caldera. The name of the proposed port development is Puerto Santo Domingo.

For the first seven years of full operation, Santo Domingo will have an annual average copper production of approximately 106,400 tonnes. The LOM average production is 68,100 tonnes of copper per year over a period of approximately 19 years. The total LOM copper production is estimated at approximately 1.3 million tonnes.

For the first seven years of operation, the annual average iron concentrate production is estimated to be 3.7 million dmt. Over the LOM, the iron concentrate production is estimated at an annual average of 3.6 million dmt, with a total estimated production of approximately 68.4 million dmt.

MINERAL RESERVE ESTIMATE

The updated Mineral Reserve estimate as at March 31, 2024, was prepared by Clay Craig, P.Eng., Capstone Copper. Based on the Mineral Resource estimate, a standard methodology for pit limit analysis, mining sequence, and cut-off grade optimization, including application of mining dilution, process recovery, economic criteria and physical mine and plant operating constraints, has been followed to design the open pit mines and determine the Mineral Reserve estimate for each deposit. The Mineral Reserves are summarized in the following table.

|

Mineral Reserve Estimate as at March 31, 2024 |

|||||||

|

Reserve Category |

Grade |

Contained Metal |

|||||

|

Tonnage |

Cu (%) |

Fe (%) |

Au (g/t) |

Cu (kt) |

Fe (Mt) |

Au (koz) |

|

|

Proven Reserves |

130.9 |

0.52 |

27.2 |

0.07 |

674.5 |

12.6 |

291 |

|

Probable Reserves |

305.1 |

0.25 |

26.2 |

0.04 |

760.7 |

55.8 |

346 |

|

Total Reserves |

436.1 |

0.33 |

26.5 |

0.05 |

1,435.2 |

68.4 |

637 |

Mineral Reserve Estimate Notes:

- Mineral Reserves are reported as constrained within Measured and Indicated Resources and pit designs optimized using the following economic and technical parameters: metal prices of US$3.75/lb Cu, US$1,400/oz Au and Fe prices ranging from US$69/dmt to US$114.51/dmt based on the Fe grade in concentrate (net of Fe concentrate transport costs); average recovery to concentrate is 90.1% for Cu and 56.3% for Au, with magnetite concentrate recovery varying on a block-by-block basis; copper concentrate treatment charges of US$80/dmt, U$0.08/lb of copper refining charges, US$5.0/oz of gold refining charges, US$40/wmt and US$25.75/dmt for shipping copper and iron concentrates respectively; waste and ore mining cost of $1.55/t and process and G&A+SUSEX of US$9.77/t processed; average pit slope angles that range from 36.3° to 47.9°; a 2% royalty rate assumption and an assumption of 100% mining recovery.

- Rounding as required by reporting standards may result in apparent summation differences between tonnes, grade and contained metal content.

- Tonnage measurements are in metric units. Copper and iron grades are reported as percentages, gold as grams per tonne. Contained gold ounces are reported as troy ounces, contained copper as million pounds and contained iron as metric million tonnes.

MINERAL RESOURCE ESTIMATE

Following is the current Mineral Resource Estimate as at March 31, 2024.

|

Category |

Deposit |

Mt |

NSR ($/t) |

Cu (%) |

Fe (%) |

Au (g/t) |

Cu kt |

Fe Mt |

Au Koz |

|

Measured |

Santo Domingo |

134 |

46 |

0.51 |

26.9 |

0.07 |

679 |

36 |

293 |

|

Indicated |

Santo Domingo + Iris Norte |

372 |

33 |

0.24 |

25.4 |

0.03 |

892 |

95 |

405 |

|

Estrellita |

41 |

24 |

0.32 |

– |

0.03 |

133 |

– |

44 |

|

|

Sub-Total |

413 |

32 |

0.25 |

n/a |

0.03 |

1,025 |

95 |

449 |

|

|

Total Measured and Indicated |

547 |

35 |

0.31 |

n/a |

0.04 |

1,704 |

131 |

742 |

|

|

Inferred |

Santo Domingo + Iris Norte |

203 |

28 |

0.19 |

22.5 |

0.03 |

384 |

46 |

171 |

|

Estrellita |

27 |

25 |

0.34 |

– |

0.03 |

93 |

– |

29 |

|

|

Total Inferred |

230 |

28 |

0.21 |

n/a |

0.03 |

477 |

46 |

200 |

|

Mineral Resource Estimate Notes:

- Mineral Resources in this document are reported inclusive of Mineral Reserves. Mineral Resources that are not Mineral Reserves do not have demonstrated economic viability.

- The average Iron grades for the Project (Total Indicated, Total Measured plus Indicated, and Total Inferred Resources) cannot be calculated because Estrellita does not contain iron resources.

- Notes specific to the Mineral Resources for the Santo Domingo and Iris Norte deposits: a. Mineral Resources for SD include Iris. b. Mineral Resources are reported using a net smelter return (NSR) cut-off value of US$9.85/t. NSR is calculated using average long-term prices of US$4.10/lb Cu, US$1,600/oz Au, and Fe prices that depend on the expected grade of the Fe concentrate (US$94.75/dmt or $129.77/dmt or $140.26/dmt Fe concentrate). c. Mineral Resources are constrained by preliminary pit shells derived using a Lerchs-Grossmann algorithm and the following assumptions: pit slopes 36.3°- 47.9°; mining cost is calculated using a function that depends on where the material comes from (Santo Domingo or Iris Norte) and its destination (dumps, plant or stock); processing cost based on Fe concentrate routing code (including G&A costs); processing recovery based in the recovery equations for copper, gold, and iron as detailed above.

- Notes specific to the Mineral Resources for the Estrellita deposit: a. Mineral Resources are reported using an NSR cut-off value of US$9.63/t. NSR is calculated using average long-term prices of US$4.10/lb Cu and US$1,600/oz Au. b. Only copper, and gold were considered in the NSR calculation; iron was excluded. c. Mineral Resources are constrained by preliminary pit shells generated using a Lerchs-Grossmann algorithm and the following assumptions: pit slopes 43º; mining cost of US$1.55/t, processing cost of US$9.46/t (including G&A cost); processing recovery are calculated based in the recovery curves for copper and gold.

- Rounding as required by reporting standards may result in apparent summation differences.

- Tonnage measurements are in metric units. Copper and iron are reported as percentages (%) and gold as grams per tonne (g/t).

For this update, Capstone undertook significant revisions and improvements to the geological models (lithology and oxidation models), the domaining strategy and the estimation scheme for both deposits. Two block models, one for Santo Domingo – Iris Norte and one for Estrellita were created incorporating the new geological modelling and an updated drill hole database that included the more recent drillholes from the Project. All grade interpolation was performed using ordinary kriging and an NSR was calculated using updated recovery curves for Cu, Au and Fe, and updated metal prices and costs. Whittle shells were used to constrain the final Mineral Resource estimates.

When comparing only the 2024 Mineral Resources for Santo Domingo and Iris Norte compared with the 2020 Feasibility Study, the update has resulted in higher Cu and Au grades, slightly lower Fe grades, and a slight increase in an additional 5% to 15% metal in Measured and Indicated and approximately two to four times more metal in Inferred Resources.

Readers are advised that Mineral Resources are not Mineral Reserves and do not have demonstrated economic viability. Mineral Resource estimates do not account for mineability, selectivity, mining loss and dilution. These Mineral Resource estimates include inferred Mineral Resources that are normally considered too speculative geologically to have economic considerations applied to them that would enable them to be categorized as Mineral Reserves. Even though test mining has been undertaken in areas with Measured and Indicated class Mineral Resources, there is no certainty that Inferred Mineral Resources will be converted to Measured and Indicated categories through further drilling, or into Mineral Reserves, once economic considerations are applied.

MINE PRODUCTION SCHEDULE

The cash flow model is supported by a mine plan developed to an annual level of detail, which is available in Exhibit 1 at the end of this release. Approximately 45 million tonnes of material would be pre-stripped prior to start-up of operations and used in the construction of the TSF starter dam. The overall strip ratio for the LOM is 2.5:1.

PROCESS DESCRIPTION

The Santo Domingo process broadly consists of the following stages: crushing, grinding, copper flotation, magnetite recovery, copper dewatering and load-out, magnetite pumping and dewatering, tailings dewatering and storage.

The primary crushing plant will process run of mine («ROM») ore feed in a gyratory crusher. A belt feeder transfers the ore from crusher area to the stockpile feed conveyor, and ultimately discharges fresh ore over a covered conical coarse ore stockpile. The stockpile allows ore reclaim using four apron feeders located within the reclaim tunnels (two trains of two feeders), which feed two parallel grinding circuits via dedicated conveyors.

Each grinding circuit consists of one 18 MW autogenous grinding mill («AG mill»), one pebble AG mill discharge screen, two pebble crushers (duty & standby), one cyclone cluster and one ball mill. The AG mill product slurry discharges over a horizontal single deck vibrating screen for pebble washing and transferring of pebbles to pebble conveyors and then to pebble crushing. Crushed pebbles report to the AG mill feed conveyor.

There is the option of bypassing the pebble crushers and recycling uncrushed material to the AG mill using the same belt conveyor system, when required. Also, a belt plow mechanism is available on the conveyors for purging pebbles to grade to aid grind-out of mills when required.

The AG mill screen undersize feeds the 9 MW variable speed ball mill and discharges into the grinding cyclone cluster feed box, where it is mixed with the ball mill product and is pumped to a cluster of 33″ classification cyclones. Cyclone underflow reports by gravity to the ball mill and cyclone overflow feeds the downstream copper flotation circuit.

Copper flotation consists of conventional rougher cell flotation, regrinding and classification, with Jameson Cells used in the cleaner scalper, cleaner scavenger, and re-cleaner stages. The rougher flotation stage recovers both copper minerals and pyrite minerals. The cleaner circuit selectively recovers copper sulphides and pyrite preferentially reports to the cleaner scavenger tail stream. There is allowance in the design for future installation of a pyrite recovery circuit to recover pyrite that contains cobalt. Final copper concentrate is pumped to downstream copper thickening and dewatering prior to stockpiling and load-out.

The iron concentrate plant is designed to produce two simultaneous products, determined by the nature of the magnetite mineral: a) a higher iron grade product («high grade concentrate»), and; b) a lower iron grade («low grade concentrate»).

A detailed Mine Production Summary and Plant Feed Production Schedule showing tonnes processed, grades and recoveries is available in Exhibit 1 at the end of this release.

The tailings storage system will consist of a tailings storage facility («TSF») located approximately 2 kilometres southeast of the proposed process plant. The TSF is designed to store approximately 361 million tonnes of high density thickened tailings, which is sufficient capacity for the approximately 19 years of the mine life. Storage of both desalinated and process water is proposed in lined ponds near the plant site. Water make-up is proposed to be desalinated water.

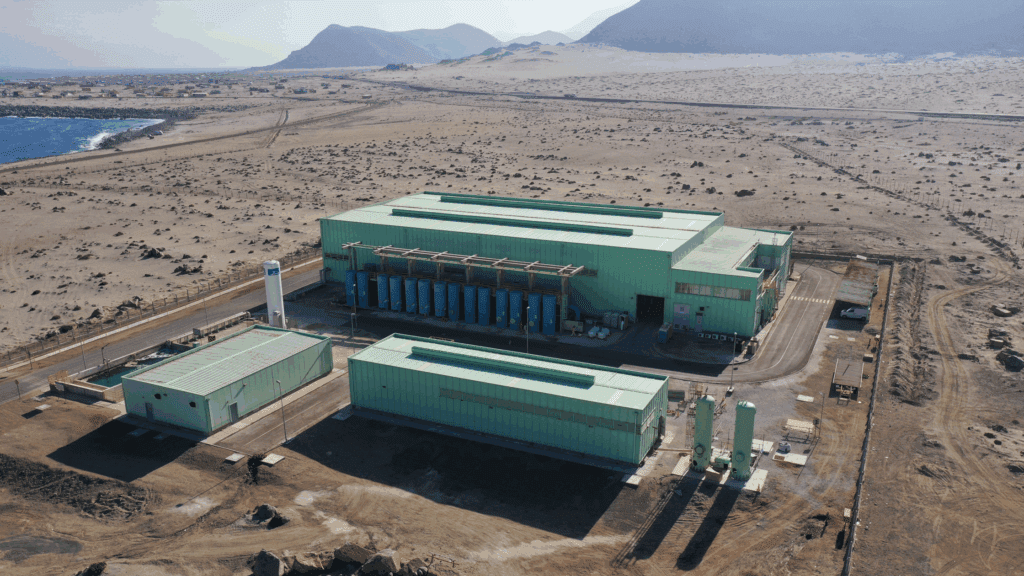

OFFSITE INFRASTRUCTURE AND SERVICES

The 2024 FS includes 100% of the capital requirements for a greenfield port in the Punta Roca Blanca area («Puerto Santo Domingo») on the coast 43 kilometres north of Caldera in the Atacama Region (Region III). The port facility is designed to accommodate the maximum throughput requirements of 5.4 million tpa of magnetite concentrate and 0.72 million tpa of copper concentrate, considering the Santo Domingo Project requirements and the future Mantoverde operation requirements.

The planned route for transporting cargo, staff and equipment to the Santo Domingo mine-plant site is from the south of the mine site by Route C-17 and from the north by Route C-13. Capstone has commenced & partially completed construction of approximately 18.5 km of the C-17 bypass road, to reroute this public highway around the mine-plant project site. The closest commercial airport is the Desierto de Atacama Airport, 113 km south from Chañaral, which has regular scheduled flights to Santiago. The closest airport to the Santo Domingo site is the El Salvador Airport, a private airport, 44 km from the mine-plant site.

WATER AND CONCENTRATE TRANSPORT

The process water required by the Santo Domingo operation will be produced by a desalination plant located at the port. Capstone has held detailed discussions with water supply companies to confirm interest in supplying desalinated water to the operation, from a facility at the port or from another location. The current plan is that a build-own-operate-transfer (BOOT) contractor will construct and operate the sea water intake, reverse osmosis desalination plant and brine return system at the port and the desalinated water pipeline as part of the BOOT contract. Alternatives under consideration are the purchase of desalinated water from an existing plant, from a plant that is planned to be built in the Atacama Region for multiuser supply, or, as part of a district integration opportunity, from a potential expansion to the desalination plant supporting Capstone’s nearby Mantoverde operation.

A magnetite concentrate pipeline will transport magnetite concentrate from the process plant to the filter plant at the port via a pipeline starting at an elevation of 1,027 masl and ending at the port at an elevation of 16 masl. Water recovered from the magnetite concentrate filtering process at the port will also be recycled and reused. The copper concentrate will be trucked from the site to Puerto Santo Domingo.

Both the water and the concentrate pipelines will use the same permitted right-of-way and will run parallel to existing roads for the majority of the distance from the mine area to the port. The pipeline route will largely follow the valleys with the single route high point located approximately 45 kilometres from the mine site near the Mantoverde mine operation.

POWER

Santo Domingo’s mine and port sites will be connected to the national grid system at local substations near the facilities. The estimated peak demand for the mine and port is 123 MW. Capstone intends to enter into a long-term power purchase agreement (PPA) with a significant renewable energy component with one of the major power companies that operate on the national grid and supply several of Chile’s major mining companies, including our Mantoverde and Mantos Blancos mines.

INITIAL CAPITAL COST ESTIMATE

The initial capital costs for the Santo Domingo Cu-Fe-Au Mine have been estimated at $2.315 billion as shown in the following table. This reflects a total capital intensity of approximately $21,900 per tonne of annual copper equivalent production over the life of mine. This estimate is based upon a constant foreign exchange rate of 800 Chilean Pesos («CLP») to US$1.00 during the development period and for the LOM.

|

INITIAL CAPITAL COST ESTIMATE (by area) |

($ millions) |

|

Mine |

370.3 |

|

Processing plant |

485.6 |

|

Tailings and water reclaim |

66.7 |

|

Plant infrastructure |

144.4 |

|

Port & port infrastructure |

283.4 |

|

External infrastructure |

150.5 |

|

Total Direct Cost |

1,500.9 |

|

Indirect costs |

413.9 |

|

Owner costs |

108.9 |

|

Contingency (~15%) |

291.0 |

|

Total Indirect Costs |

813.8 |

|

TOTAL INITIAL CAPITAL COSTS |

2,314.7 |

Mine pre-production pre-strip costs are estimated at $70 million and are included in the «Mine» initial capital cost estimate. External infrastructure largely relates to the Fe magnetite concentrate pipeline, power infrastructure, and roads. LOM sustaining capital and deferred stripping, estimated at $441 million and $888 million, respectively, over the approximate 19-year mine life, are not included in the above figure. LOM Mine closure costs have been estimated at $124 million and have been included in the financial model. In 2019, the Closure Plan was formally approved by the Chilean authorities.

SUMMARY OF OPERATING COST ESTIMATE

As shown, the total by-product C1 cash costs8 over LOM are estimated at $0.33 per pound of payable copper produced, when including iron and applicable gold credits. The co-product LOM C1 cash costs9 are estimated at approximately $1.59 per pound of payable copper equivalent and $32.99 per tonne of magnetite concentrate equivalent produced.

|

Total Project Operating Costs10 |

|||

|

LOM Total ($ millions) |

LOM Average ($/t milled) |

LOM C1 Cash Costs11 ($/lb payable Cu) |

|

|

Mining |

1,588 |

3.64 |

0.58 |

|

Processing |

3,708 |

8.51 |

1.35 |

|

G&A |

549 |

1.26 |

0.20 |

|

Sub-Total |

$5,845 |

$13.41 |

$2.13 |

|

By-Product Credits |

|

|

(2.12) |

|

Treatment and Refining Charges and Selling Costs |

|

|

0.32 |

|

TOTAL C1 cash costs12 per pound of payable copper produced |

|

|

$0.33 |

Mining costs in the above table exclude deferred stripping (included as capital expenditures) of $888 million ($2.04/t milled) and pre-stripping (included in initial capital expenditures) of $70 million. Mining costs including deferred stripping are $1.57 per tonne moved over the life-of-mine.

PERMITTING

In July 2015, Capstone received approval of the Environmental Impact Assessment («EIA») for the mine, and later, in 2020, for the desalination plant. The Maritime Concession was approved in March 2016. In July 2017, long lead-time permit applications required to start construction were submitted, and they have all since been received, including formal approval of the Mine Closure Plan received in 2019. The permits received include Mine Development, Plant, Tailings Storage Facility, Waste Rock Storage, Flora and Fauna Rescue, Change of Land-Use and High Voltage Connection.

Santo Domingo maintains 15 years of tax stability post commencement of commercial production under the previous taxation legislation in Chile as a result of Decree Law No. 600 («DL 600»).

8 C1 cash costs are net of magnetite iron and gold by-product credits and selling costs. These are Non-GAAP performance measures; please see «Non-GAAP and Other Performance Measures» at the end of this news release.

9 C1 cash costs on a co-product basis consist of mining costs, processing costs, mine-level G&A, gold revenue credit, and refining charges over payable copper equivalent pounds (copper plus magnetite) or magnetite equivalent tonnes (magnetite plus copper). These are Non-GAAP performance measures; please see «Non-GAAP and Other Performance Measures» at the end of this news release.

10 These are Non-GAAP performance measures; please see «Non-GAAP and Other Performance Measures» at the end of this news release. Totals may not sum due to rounding.

11 These are Non-GAAP performance measures; please see «Non-GAAP and Other Performance Measures» at the end of this news release.

12 C1 cash costs are net of magnetite iron and cash gold by-product credits and selling costs. These are Non-GAAP performance measures; please see «Non-GAAP and Other Performance Measures» at the end of this news release.

COMMODITY PRICING

The updated 2024 feasibility study assumes analyst consensus long-term commodity price assumptions for copper, iron ore, and gold.

Copper

Capstone markets copper concentrate from its four mining operations. Santo Domingo copper concentrate is generally considered clean and low in impurities (deleterious or penalty elements). Capstone foresees substantial demand from trading companies that specialize in blending complex materials with cleaner concentrates. These companies typically prefer concentrates like Santo Domingo’s due to their compatibility with blending processes and enhanced value proposition. High-quality concentrates are coveted by both smelters and traders alike. This further supports the expected strong demand for Santo Domingo’s copper concentrate in the market.

The analyst consensus long-term copper price was determined to be $4.10/lb which is slightly below the current spot price and compares with the five-year trailing average of approximately $3.68/lb.

Iron

Santo Domingo will produce three products, a 62%, 65%, and 67% iron concentrate product. The iron concentrate forecast in the production schedule is a typical pellet feed currently used in pellet plants. Magnetite is the predominant mineral. The iron concentrate grade is high and the low alumina (Al2O3) and low phosphorus (P) make the concentrate suitable for most pellet plants. Suitability and demand for this pellet feed will be considered in the context of increasing use of pellets in iron making, the increased use of higher-grade concentrate generally and as a premium additive to sinter plants by blending. Iron ore concentrate will be produced for shipment overseas in capesize vessels to iron and steel makers.

The analyst consensus long-term 62% and 65% (CFR China) prices were determined to be $85/t and $110/t, respectively. These compare to current spot prices of approximately $100/t and $120/t, and averages over the last five years, of approximately $110/t and $129/t, respectively. An additional premium of $10/t (CFR-China) is assumed for the Project’s 67% Fe product. The financial model assumes a $25/t FOB Chile freight charge based on a long-term analysis of trans-oceanic chartering costs for the Chile-to-China route. As a result, Santo Domingo’s realized price for its 65% iron ore magnetite product is assumed to be $85/t FOB Santo Domingo port.

OPPORTUNITIES

The company plans to continue to progress several value enhancement initiatives within the Mantoverde-Santo Domingo district that are not yet incorporated into the base case 2024 FS, which so far only considers the processing of copper and iron ore concentrate at Santo Domingo.

Copper Oxides

Capstone plans to progress drilling and studies regarding the processing of Santo Domingo’s oxide material using Mantoverde’s excess SX-EW capacity. To date, oxide materials have been recognized in the shallower portions of the Santo Domingo, Iris Norte, and Estrellita sulfide orebodies. Currently, these oxides are considered as waste material in the Santo Domingo 2024 FS. Meanwhile, only approximately two thirds of processing capacity is being used at Mantoverde’s SX-EW cathode copper plant. Exploration efforts at Santo Domingo will target a potential 80-100 million tonnes of oxide material, which could add up to 10 thousand tonnes per annum of copper production.

Cobalt

A district cobalt plant for the Mantoverde-Santo Domingo district is designed to unlock cobalt production while reducing sulphuric acid consumption and increasing heap leach copper production. The cobalt recovery process comprises a pyrite flotation step to recover cobaltiferous pyrite from the tailings streams at Santo Domingo and Mantoverde and redirect it to the dynamic heap leach pads, which will be upgraded to a bio-leach configuration through the addition of an aeration system. The pyrite oxidizes in the leach pads and the solubilized cobalt is recovered via an ion exchange plant treating a bleed stream from the copper solvent extraction plant. The approach has been successfully demonstrated at the bench scale, and onsite piloting commenced in January 2024 at Mantoverde.

As currently envisioned, a smaller capacity countercurrent ion-exchange plant will initially treat cobalt by-product streams from Mantoverde producing up to 1,500 tonnes per annum of cobalt, and following sanctioning of the Santo Domingo project, the facility will be expanded to accommodate by-product streams from Santo Domingo. In line with this, Santo Domingo has initiated a Feasibility Study to assess the optimum process configuration for the pyrite flotation and pumping transportation facilities needed to transport pyrite concentrate to Mantoverde’s leach facilities.

Santo Domingo Port and Mantoverde Copper Concentrate

Capstone’s Mantoverde mine will be able to use the planned Santo Domingo port to ship concentrate. The planned Santo Domingo port is located 65 kilometres from Mantoverde when compared to Puerto Angamos, the current planned shipping destination, 475 kilometres away. This decrease in trucking distance is expected to reduce Mantoverde transport costs by up to $10 million per annum. The planned Santo Domingo port is expected to have sufficient scale to handle capsize vessels suitable for large cargo, including Santo Domingo-Mantoverde copper concentrate, iron ore, district cobalt production, and the potential for sulphuric acid handling.

Exploration in the Mantoverde-Santo Domingo District

Capstone has significant untapped exploration potential within Mantoverde-Santo Domingo district. At Mantoverde, there are 0.3 billion tonnes of Measured & Indicated and 0.6 billion tonnes of Inferred sulphide resources not in reserves. At Santo Domingo, there are 0.1 billion tonnes of Measured & Indicated and 0.2 billion tonnes of Inferred sulphide resources not in reserves. Capstone intends to progress its exploration strategy, starting with the recently announced two-year $25 million exploration program at Mantoverde, to service its two eventual processing centers between Mantoverde and Santo Domingo.

Subsequent to the quarter ended June 30, 2024, Capstone entered into a binding share purchase agreement (the «SPA») with Inversiones Alxar S.A. («Alxar») and Empresas COPEC S.A. («EC»), collectively the «Sellers» to acquire 100% of Compania Minera Sierra Norte S.A. («Sierra Norte»). The Sierra Norte land package covers over 7,000 hectares in Region III, Chile and hosts an historic resource (non NI 43-101 compliant) of approximately 100Mt at 0.45% CuT13 with exploration upside. Sierra Norte is located approximately 20 kilometres northwest of the Santo Domingo Project and represents an opportunity to potentially be a future sulphide feed source for Santo Domingo, extending the higher-grade copper sulphide life. Under the terms of the SPA, Capstone will pay the Sellers $40 million payable in share consideration. Closing is expected within 1-week.

13 This is an historic resource (not 43-101 compliant). Please refer to the notes outlined in Exhibit 2 for more details.

ENVIRONMENTAL AND SOCIAL BENEFITS

Capstone’s Sustainable Development Strategy reflects the Company’s core values and commitment to responsible mining practices. Environmental and social benefits embedded within the updated Santo Domingo 2024 FS include:

- The base case Santo Domingo plan is expected to produce copper and a high-quality iron ore magnetite concentrate, supporting the world’s decarbonization efforts. Capstone is also working to add a third critical metal in cobalt to Santo Domingo’s production profile.

- Santo Domingo is expected to generate over 1,000 jobs. Training programs and strategic partnerships with technical schools in nearby Chañaral and Diego de Almagro are also planned.

- Capstone expects to enter into a PPA for Santo Domingo’s power requirements that contains a significant renewable energy component. Capstone is targeting greater than 90% renewable electricity across our portfolio by 2030.

- The mining fleet features electric shovels, similar to the electric shovels at Capstone’s Mantoverde mine which reduce emissions relative to diesel-powered equipment.

- The mine plan has a lower strip ratio when compared to the previous study, which translates to less waste per tonne of ore, and less mined material per tonne of metal.

- The updated processing plant features an approximate 40% footprint reduction compared to the prior plan, minimizing footprint associated earthworks and environmental impacts.

- The covered primary stockpile and rotainers for copper concentrate shipment are examples of best-practice dust suppression capabilities.

- The processing flowsheet features fully autogenous grinding, reducing steel consumption.

- High density thickeners reduce water consumption by maximizing the recycling of water and minimizing evaporation losses in the tailings dam, ultimately reducing requirements for desalinated water and pumping.

- The tailings storage facility design exceeds the Chilean standards and is aligned with Capstone’s corporate commitment to adopt the Global Industry Standard on Tailings Management. Furthermore, the potential future cobalt production would convert waste in the tailings stream, an environmental liability, into metal, an economic asset.

- The Company plans to support the local community of Diego de Almagro with 10 litres per second of potable water coming from the desalination plant.

- The planned Santo Domingo multi-user port will provide benefits to the local region. In addition, trucking emissions for transporting Mantoverde’s copper concentrate will be significantly reduced.

- The updated 2024 FS outlines over $2 billion in-country taxes paid in Chile over the life of mine.

NATIONAL INSTRUMENT 43-101

A National Instrument 43-101 («NI 43-101») Technical Report will be prepared to summarize the results of the 2024 Feasibility Study by the Qualified Persons and will be filed on SEDAR+ within 45 days of this news release.

Readers are cautioned that the conclusions, projections and estimates set out in this news release are subject to important qualifications, assumptions and exclusions, all of which will be detailed in the 2024 technical report. To fully understand the summary information set out above, the 2024 technical report that will be filed on SEDAR+ at www.sedarplus.ca should be read in its entirety.

QUALIFIED PERSONS

Peter Amelunxen, P.Eng., Senior Vice President, Technical Services of Capstone Copper, a Qualified Person («QP»), as defined by NI 43-101 reviewed and approved the content of this news release that is based on the 2024 technical report.

About Capstone Copper Corp.

Capstone Copper Corp. is an Americas-focused copper mining company headquartered in Vancouver, Canada. We own and operate the Pinto Valley copper mine located in Arizona, USA, the Cozamin copper-silver mine located in Zacatecas, Mexico, the Mantos Blancos copper-silver mine located in the Antofagasta region, Chile, and 70% of the Mantoverde copper-gold mine, located in the Atacama region, Chile. In addition, we own the fully permitted Santo Domingo copper-iron-gold project, located approximately 30 kilometres northeast of Mantoverde in the Atacama region, Chile, as well as a portfolio of exploration properties in the Americas.

Capstone Copper’s strategy is to unlock transformational copper production growth while executing on cost and operational improvements through innovation, optimization and safe and responsible production throughout our portfolio of assets. We focus on profitability and disciplined capital allocation to surface stakeholder value. We are committed to creating a positive impact in the lives of our people and local communities, while delivering compelling returns to investors by responsibly producing copper to meet the world’s growing needs.

Further information is available at www.capstonecopper.com

CAUTIONARY NOTE REGARDING FORWARD-LOOKING STATEMENTS

This document may contain «forward-looking information» within the meaning of Canadian securities legislation and «forward-looking statements» within the meaning of the United States Private Securities Litigation Reform Act of 1995 (collectively, «forward-looking statements»). These forward-looking statements are made as of the date of this document and the Company does not intend, and does not assume any obligation, to update these forward-looking statements, except as required under applicable securities legislation.

Forward-looking statements relate to future events or future performance and reflect Company management’s expectations or beliefs regarding future events and include, but are not limited to, statements with respect to the estimation of mineral reserves and mineral resources, the conversion of mineral resources to mineral reserves, the ability to successfully complete the strategic review process, the ability to further enhance the value of the project, the expected timing for commencement of construction of the Santo Domingo project, the future validity of the DL600, our ability to fund future exploration activities, the market for project debt, Capstone’s ability to raise its equity contribution to the project, the realization of mineral reserve estimates, the timing and amount of estimated future production, costs of production, capital and construction expenditures, success of mining operations, success of mineral exploration, environmental risks, the timing of the receipt of permits, the timing and terms of a power purchase agreement, unanticipated reclamation expenses, title disputes or claims and limitations on insurance coverage. In certain cases, forward-looking statements can be identified by the use of words such as «plans», «expects» or «does not expect», «is expected», «outlook», «budget», «scheduled», «estimates», «forecasts», «intends», «anticipates» or «does not anticipate», or «believes», or variations of such words and phrases or statements that certain actions, events or results «may», «could», «would», «might» or «will be taken», «occur» or «be achieved» or the negative of these terms or comparable terminology. In this document certain forward-looking statements are identified by words including «explore», «potential», «will», «scheduled», «plan», «planned», «estimates», «estimated», «estimate», «projections», «projected», «await receipt» and «expected». Forward-looking statements are based on a number of assumptions which may prove incorrect, including, but not limited to, the development potential of the Santo Domingo project and current and future commodity prices and exchange rates. By their very nature forward-looking statements involve known and unknown risks, uncertainties and other factors which may cause the actual results, performance or achievements of the Company to be materially different from any future results, performance or achievements expressed or implied by the forward-looking statements. Such factors include, among others, changes in project parameters as plans continue to be refined; future prices of commodities; possible variations in mineral resources and reserves, grade or recovery rates; accidents; dependence on key personnel; labour pool constraints; labour disputes; availability of infrastructure required for the development of mining projects; delays in obtaining governmental approvals, financing or in the completion of development or construction activities; objections by the communities or environmental lobby of the Santo Domingo mine and associated infrastructure and other risks of the mining industry as well as those factors detailed from time to time in the Company’s interim and annual financial statements and management’s discussion and analysis of those statements, all of which are filed and available for review on SEDAR+ at www.sedarplus.ca. Although the Company has attempted to identify important factors that could cause actual actions, events or results to differ materially from those described in forward-looking statements, there may be other factors that cause actions, events or results not to be as anticipated, estimated or intended. There can be no assurance that forward-looking statements will prove to be accurate, as actual results and future events could differ materially from those anticipated in such statements. Accordingly, readers should not place undue reliance on forward looking statements.

Non-GAAP and Other Performance Measures

The Company uses certain performance measures in its analysis. «C1 Cash Costs» and «Total Project Operating Cost» are Non-GAAP performance measures. These Non-GAAP performance measures are included in this document because these statistics are key performance measures that management uses to monitor performance, to assess how the Company is performing, and to plan and assess the overall effectiveness and efficiency of mining operations. These performance measures do not have a standard meaning within IFRS and, therefore, amounts presented may not be comparable to similar data presented by other mining companies. These performance measures should not be considered in isolation as a substitute for measures of performance in accordance with IFRS.

Exhibit 1: Detailed Cash Flow Model and Select Key Assumptions

|

|

Unit |

LOM |

-3 |

-2 |

-1 |

1 |

2 |

3 |

4 |

5 |

6 |

7 |

8 |

9 |

10 |

11 |

12 |

13 |

14 |

15 |

16 |

17 |

18 |

19 |

|

|

||||||||||||||||||||||||

|

Production Summary |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Mineral Resource Mined to Plant |

kt |

377,303 |

— |

— |

— |

19,939 |

26,279 |

21,319 |

25,086 |

26,278 |

23,726 |

23,722 |

16,311 |

18,838 |

23,726 |

18,234 |

17,929 |

21,884 |

11,486 |

15,140 |

18,352 |

16,641 |

17,588 |

14,826 |

|

Mineral Resource Mined to Stockpile |

kt |

58,753 |

— |

1,149 |

5,126 |

1,106 |

989 |

74 |

9,251 |

6,623 |

13,522 |

6,634 |

1,928 |

2,104 |

8,559 |

692 |

995 |

— |

— |

— |

— |

— |

— |

— |

|

Waste Mined |

kt |

1,074,757 |

— |

8,859 |

26,321 |

66,716 |

62,260 |

62,080 |

50,408 |

43,729 |

51,137 |

58,265 |

62,652 |

62,960 |

57,480 |

66,275 |

60,415 |

61,860 |

56,808 |

62,241 |

66,139 |

54,252 |

24,250 |

9,652 |

|

Mineral Resource Rehandled |

kt |

58,753 |

— |

— |

— |

— |

— |

4,962 |

1,267 |

— |

— |

— |

7,480 |

4,887 |

— |

5,491 |

5,862 |

1,841 |

12,240 |

8,586 |

— |

2,320 |

1,400 |

2,418 |

|

Throughput |

ktpd |

n/a |

— |

— |

— |

54.6 |

72.0 |

72.0 |

72.2 |

72.0 |

65.0 |

65.0 |

65.2 |

65.0 |

65.0 |

65.0 |

65.2 |

65.0 |

65.0 |

65.0 |

50.3 |

51.9 |

52.0 |

47.2 |

|

Resource Sent to Mill |

kt |

436,056 |

— |

— |

— |

19,939 |

26,279 |

26,281 |

26,353 |

26,278 |

23,726 |

23,722 |

23,791 |

23,725 |

23,726 |

23,725 |

23,791 |

23,725 |

23,726 |

23,725 |

18,352 |

18,961 |

18,988 |

17,243 |

|

Cu Head Grade |

% |

0.33% |

— |

— |

— |

0.50% |

0.59% |

0.48% |

0.49% |

0.43% |

0.45% |

0.39% |

0.26% |

0.22% |

0.30% |

0.33% |

0.31% |

0.22% |

0.20% |

0.29% |

0.20% |

0.12% |

0.11% |

0.13% |

|

Au Head Grade |

g/t |

0.05 |

— |

— |

— |

0.07 |

0.08 |

0.07 |

0.07 |

0.06 |

0.07 |

0.06 |

0.04 |

0.03 |

0.04 |

0.05 |

0.05 |

0.03 |

0.03 |

0.04 |

0.03 |

0.02 |

0.01 |

0.01 |

|

Fe Head Grade |

% |

26.5% |

— |

— |

— |

25.0% |

29.0% |

26.4% |

29.4% |

30.0% |

32.0% |

30.7% |

26.6% |

26.7% |

28.4% |

25.8% |

23.2% |

21.4% |

21.9% |

21.2% |

24.1% |

25.8% |

26.4% |

27.5% |

|

Cu Recovery |

% |

90.1% |

— |

— |

— |

90.6% |

91.6% |

91.2% |

91.0% |

88.5% |

89.0% |

90.4% |

90.0% |

89.5% |

89.7% |

90.1% |

90.0% |

89.4% |

88.7% |

90.1% |

90.4% |

89.7% |

88.7% |

89.2% |

|

Au Recovery |

% |

64.7% |

— |

— |

— |

70.2% |

71.0% |

68.9% |

68.1% |

66.0% |

66.0% |

64.8% |

60.6% |

58.9% |

61.3% |

62.1% |

62.5% |

59.5% |

58.2% |

62.6% |

58.8% |

57.1% |

57.1% |

53.0% |

|

Fe Recovery |

% |

59.2% |

— |

— |

— |

26.9% |

48.1% |

59.7% |

56.6% |

57.0% |

56.2% |

51.9% |

68.0% |

70.7% |

62.1% |

43.8% |

46.0% |

67.5% |

53.3% |

38.6% |

64.4% |

88.7% |

87.5% |

93.2% |

|

Cu Production |

kt |

1,293.1 |

— |

— |

— |

90.8 |

142.0 |

114.9 |

118.1 |

98.9 |

95.4 |

84.4 |

56.0 |

47.1 |

64.6 |

70.5 |

67.1 |

47.3 |

42.2 |

61.6 |

33.0 |

20.7 |

19.2 |

19.4 |

|

Au Production |

koz |

412 |

— |

— |

— |

31 |

47 |

38 |

39 |

32 |

33 |

27 |

18 |

13 |

21 |

23 |

22 |

14 |

12 |

18 |

10 |

6 |

5 |

4 |

|

Fe Production |

Mt |

68.4 |

— |

— |

— |

1.3 |

3.7 |

4.1 |

4.4 |

4.5 |

4.3 |

3.8 |

4.3 |

4.5 |

4.2 |

2.7 |

2.5 |

3.4 |

2.8 |

1.9 |

2.8 |

4.3 |

4.4 |

4.4 |

|

Cu Payable |

kt |

1,242.9 |

— |

— |

— |

87.5 |

136.9 |

110.7 |

113.6 |

95.0 |

91.7 |

81.1 |

53.7 |

45.2 |

62.0 |

67.7 |

64.4 |

45.4 |

40.4 |

59.2 |

31.6 |

19.9 |

18.5 |

18.5 |

|

Cu Concentrate Grade |

% |

26.4% |

— |

— |

— |

28.3% |

28.4% |

27.6% |

27.1% |

26.5% |

26.1% |

26.0% |

25.4% |

25.1% |

25.2% |

25.2% |

25.6% |

25.5% |

25.2% |

26.1% |

25.6% |

26.4% |

25.9% |

23.7% |

|

Au Payable |

koz |

370 |

— |

— |

— |

28 |

42 |

34 |

35 |

29 |

29 |

25 |

16 |

12 |

19 |

20 |

19 |

13 |

11 |

16 |

9 |

5 |

4 |

4 |

|

Fe Payable |

Mt |

68.4 |

— |

— |

— |

1.3 |

3.7 |

4.1 |

4.4 |

4.5 |

4.3 |

3.8 |

4.3 |

4.5 |

4.2 |

2.7 |

2.5 |

3.4 |

2.8 |

1.9 |

2.8 |

4.3 |

4.4 |

4.4 |

|

Fe Concentrate Grade |

% |

65.4% |

— |

— |

— |

62.5% |

65.0% |

66.2% |

66.6% |

66.4% |

65.6% |

65.6% |

65.6% |

66.2% |

66.2% |

65.4% |

64.4% |

65.4% |

65.0% |

63.5% |

64.2% |

64.6% |

65.0% |

65.6% |

|

Revenues |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Copper Revenue |

$M |

$11,235 |

— |

— |

— |

$791 |

$1,237 |

$1,000 |

$1,027 |

$859 |

$829 |

$733 |

$486 |

$408 |

$561 |

$612 |

$582 |

$411 |

$365 |

$535 |

$286 |

$180 |

$167 |

$167 |

|

Gold Revenue |

$M |

$171 |

— |

— |

— |

$9 |

$14 |

$11 |

$11 |

$9 |

$10 |

$8 |

$6 |

$5 |

$7 |

$10 |

$17 |

$11 |

$9 |

$14 |

$7 |

$5 |

$4 |

$3 |

|

Magnetite concentrate revenue |

$M |

$5,664 |

— |

— |

— |

$84 |

$311 |

$366 |

$396 |

$406 |

$373 |

$329 |

$371 |

$408 |

$373 |

$233 |

$169 |

$275 |

$214 |

$137 |

$178 |

$278 |

$374 |

$387 |

|

Gross Revenue |

$M |

$17,069 |

— |

— |

— |

$884 |

$1,562 |

$1,378 |

$1,435 |

$1,274 |

$1,211 |

$1,070 |

$863 |

$821 |

$941 |

$855 |

$767 |

$697 |

$589 |

$686 |

$471 |

$462 |

$544 |

$558 |

|

Operating Costs |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Mine Operating Costs |

$M |

($1,588) |

— |

— |

— |

($75) |

($101) |

($73) |

($134) |

($79) |

($88) |

($69) |

($73) |

($88) |

($131) |

($91) |

($75) |

($88) |

($42) |

($73) |

($81) |

($90) |

($80) |

($56) |

|

Mill Processing Costs |

$M |

($3,708) |

— |

— |

— |

($193) |

($216) |

($211) |

($217) |

($214) |

($208) |

($202) |

($207) |

($198) |

($214) |

($204) |

($191) |

($189) |

($203) |

($196) |

($160) |

($168) |

($166) |

($152) |

|

G&A Costs |

$M |

($549) |

— |

— |

— |

($29) |

($28) |

($27) |

($27) |

($29) |

($29) |

($30) |

($30) |

($29) |

($29) |

($30) |

($29) |

($29) |

($29) |

($30) |

($29) |

($28) |

($28) |

($28) |

|

Refining Charges, Treatment Charges, Transportation Cost & Royalties |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Refining |

$M |

($194) |

— |

— |

— |

($14) |

($21) |

($17) |

($18) |

($15) |

($14) |

($13) |

($8) |

($7) |

($10) |

($11) |

($10) |

($7) |

($6) |

($9) |

($5) |

($3) |

($3) |

($3) |

|

Treatment Costs |

$M |

($342) |

— |

— |

— |

($22) |

($35) |

($29) |

($30) |

($26) |

($26) |

($23) |

($15) |

($13) |

($18) |

($20) |

($18) |

($13) |

($12) |

($16) |

($9) |

($5) |

($5) |

($6) |

|

Transport Costs |

$M |

($328) |

— |

— |

— |

($21) |

($33) |

($28) |

($29) |

($25) |

($24) |

($22) |

($15) |

($13) |

($17) |

($19) |

($18) |

($12) |

($11) |

($16) |

($9) |

($5) |

($5) |

($5) |

|

Storage & Marketing |

$M |

($15) |

— |

— |

— |

($1) |

($2) |

($1) |

($1) |

($1) |

($1) |

($1) |

($1) |

($1) |

($1) |

($1) |

($1) |

($1) |

($1) |

($1) |

($0) |

($0) |

($0) |

($0) |

|

Insurance Charges |

$M |

($5) |

— |

— |

— |

($0) |

($1) |

($0) |

($0) |

($0) |

($0) |

($0) |

($0) |

($0) |

($0) |

($0) |

($0) |

($0) |

($0) |

($0) |

($0) |

($0) |

($0) |

($0) |

|

Royalties |

$M |

($288) |

— |

— |

— |

($17) |

($30) |

($27) |

($28) |

($18) |

($15) |

($15) |

($16) |

($14) |

($11) |

($12) |

($11) |

($13) |

($10) |

($13) |

($9) |

($9) |

($10) |

($11) |

|

Cost Guarantee |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Cost Guarantee |

$M |

($11) |

— |

— |

— |

($0) |

($0) |

($0) |

($0) |

($0) |

($1) |

($1) |

($1) |

($1) |

($1) |

($1) |

($1) |

($1) |

($1) |

($1) |

($1) |

($1) |

— |

— |

|

Other Income |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Other Income |

$M |

$47 |

— |

— |

— |

$5 |

$4 |

$4 |

$4 |

$4 |

$5 |

$3 |

$3 |

$4 |

$2 |

$2 |

$2 |

$2 |

$2 |

$1 |

— |

— |

— |

— |

|

EBITDA |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

EBITDA |

$M |

$10,086 |

|

|

|

$516 |

$1,099 |

$967 |

$952 |

$870 |

$810 |

$698 |

$501 |

$462 |

$511 |

$469 |

$415 |

$346 |

$276 |

$332 |

$167 |

$152 |

$246 |

$297 |

|

Gold Streams Proceeds |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Remaining Gold Streams Proceeds |

$M |

$260 |

$28 |

$58 |

$174 |

— |

— |

— |

— |

— |

— |

— |

— |

— |

— |

— |

— |

— |

— |

— |

— |

— |

— |

— |

|

Capital Expenditures |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Initial Capital |

$M |

($2,315) |

($85) |

($744) |

($1,119) |

($366) |

— |

— |

— |

— |

— |

— |

— |

— |

— |

— |

— |

— |

— |

— |

— |

— |

— |

— |

|

Sustaining Capital |

$M |

($441) |

— |

— |

— |

($30) |

($73) |

($15) |

($34) |

($43) |

($11) |

($10) |

($19) |

($24) |

($20) |

($10) |

($45) |

($24) |

($37) |

($29) |

($9) |

($3) |

($2) |

($1) |

|

Deferred Stripping |

$M |

($888) |

— |

— |

— |

($55) |

($58) |

($81) |

($39) |

($55) |

($43) |

($68) |

($59) |

($48) |

($9) |

($46) |

($57) |

($41) |

($72) |

($52) |

($55) |

($49) |

— |

— |

|

Closure Cost |

$M |

($124) |

— |

— |

— |

— |

— |

— |

— |

— |

— |

— |

— |

— |

— |

— |

— |

($18) |

($18) |

($18) |

($18) |

($18) |

($18) |

($18) |

|

Change in Working Capital |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Change in Working Capital |

$M |

— |

— |

— |

— |

($80) |

($15) |

$10 |

($17) |

$15 |

($1) |

$7 |

($0) |

($1) |

($16) |

$12 |

$8 |

($1) |

$8 |

($7) |

$9 |

($3) |

$3 |

$70 |

|

Pre-Tax Unlevered Free Cash Flow |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Pre-Tax Unlevered Free Cash Flow |

$M |

$6,579 |

($57) |

($686) |

($945) |

($15) |

$952 |

$881 |

$861 |

$788 |

$755 |

$627 |

$423 |

$389 |

$466 |

$424 |

$322 |

$261 |

$157 |

$226 |

$95 |

$79 |

$228 |

$349 |

|

Pre-Tax Cumulative Unlevered Free Cash Flow |

$M |

$6,579 |

($57) |

($743) |

($1,688) |

($1,703) |

($751) |

$130 |

$991 |

$1,779 |

$2,534 |

$3,161 |

$3,583 |

$3,972 |

$4,438 |

$4,863 |

$5,184 |

$5,446 |

$5,602 |

$5,829 |

$5,923 |

$6,002 |

$6,231 |

$6,579 |

|

Taxes |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Unlevered Cash Taxes |

$M |

($2,020) |

— |

— |

— |

($13) |

($68) |

($51) |

($247) |

($230) |

($216) |

($199) |

($137) |

($113) |

($135) |

($140) |

($119) |

($72) |

($56) |

($72) |

($25) |

($24) |

($52) |

($50) |

|

Post-Tax Unlevered Free Cash Flow |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Post-Tax Unlevered Free Cash Flow |

$M |

$4,559 |

($57) |

($686) |

($945) |

($28) |

$884 |

$829 |

$615 |

$558 |

$540 |

$427 |

$286 |

$277 |

$331 |

$284 |

$203 |

$189 |

$101 |

$154 |

$70 |

$55 |

$176 |

$298 |

|

Post-Tax Cumulative Unlevered Free Cash Flow |

$M |

$4,559 |

($57) |

($743) |

($1,688) |

($1,717) |

($832) |

$3 |

$611 |

$1,169 |

$1,708 |

$2,136 |

$2,421 |

$2,698 |

$3,029 |

$3,313 |

$3,516 |

$3,705 |

$3,806 |

$3,960 |

$4,030 |

$4,085 |

$4,261 |

$4,559 |

|

Cost KPI’s |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

C1 (by-product basis)* |

$/lb Cu |

$0.33 |

— |

— |

— |

$1.36 |

$0.37 |

$0.04 |

$0.20 |

($0.12) |

$0.04 |

$0.13 |

($0.24) |

($0.65) |

$0.29 |

$0.89 |

$1.11 |

$0.53 |

$0.90 |

$1.46 |

$1.56 |

$0.40 |

($2.19) |

($3.45) |

|

C1 (co-product basis)** |

$/lb Cu Eq. |

$1.59 |

— |

— |

— |

$1.62 |

$1.12 |

$1.13 |

$1.29 |

$1.23 |

$1.30 |

$1.36 |

$1.64 |

$1.72 |

$1.81 |

$1.77 |

$1.78 |

$1.96 |

$2.08 |

$2.00 |

$2.53 |

$2.65 |

$2.16 |

$1.82 |

*C1 consist of mining costs, processing costs, mine-level G&A, gold revenue credit, and refining charges over payable copper equivalent pounds (copper plus magnetite)

** C1 consist of mining costs, processing costs, mine-level G&A, gold revenue credit, magnetite revenue credit, and refining charges over payable copper pounds

|

PRICE DECK & MARKETING ASSUMPTIONS |

||

|

Assumption |

Unit |

LOM |

|

Copper Price |

$/lb |

$4.10 |

|

Gold Price |

$/oz |

$1,800 |

|

62% grade magnetite Conc. Price (CFR China) |

$/t |

$85 |

|

65% grade magnetite Conc. Price (CFR China) |

$/t |

$110 |

|

67% grade magnetite Conc. Price (CFR China) |

$/t |

$120 |

|

Freight Charge (Chile-to-China) |

$/t |

$25 |

|

Chilean Peso |

CLP/USD |

800:1 |

|

Copper Treatment Charges |

$/dmt |

$70 |

|

Copper Refining Charges |

$/lb Cu |

$0.07 |

|

Gold refining charge |

$/oz |

$5 |

Exhibit 2: Sierra Norte, Historical Mineral Resources

|

Category |

Tonnes (Mt) |

CuT % |

CuS % |

Copper (kt) |

|

Carmen-Paulina |

||||

|

Measured |

7.5 |

0.47% |

0.16% |

35.5 |

|

Indicated |

63.5 |

0.46% |

0.10% |

292.0 |

|

Inferred |

25.1 |

0.40% |

0.04% |

101.5 |

|

Total |

96.1 |

0.45% |

0.09% |

429.0 |

|

|

|

|

|

|

|

Esther |

|

|

|

|

|

Measured |

0.7 |

0.42% |

0.26% |

3.0 |

|

Indicated |

3.3 |

0.40% |

0.24% |

13.3 |

|

Inferred |

0.1 |

0.35% |

0.22% |

0.3 |

|

Total |

4.1 |

0.40% |

0.24% |

16.6 |

Notes:

The Historical Mineral Resource was derived from the report «Actualización del Modelo Geológico y de la Estimación de Recursos Minerales del Proyecto Diego de Almagro» completed by Amec Foster Wheeler with an effective date on April 29, 2016 prepared for Alxar S.A. The historical estimates are strictly historical in nature and are non compliant with NI 43-101 and should not be relied upon. A qualified person has not done sufficient work to classify the historical estimates as current «mineral resources», as such term is defined in NI 43-101 and it is uncertain whether, following further evaluation or exploration work, the historical estimates will be able to report as mineral resources in accordance with NI 43-101. Capstone has not done sufficient work to classify the historical estimate as current mineral resources and is not treating the historical estimate as current mineral resources. Mineral Resources that are not Mineral Reserves do not have demonstrated economic viability. Mineral Resources reported using a cut-off grade of 0.2% with further economic extraction parameters outlined below. Mineral Resources reported by category; based on average spacing of drillholes and levels of confidence in the grade estimation. There are no more recent estimates or data available to Capstone. The Sierra Norte deposit will require further evaluation including drilling to verify the historical estimate as current mineral resources. Investors are cautioned not to place undue reliance on the historical estimates contained in this news release. Economic Parameters for Mineral Resources include the following: Copper price: $3.00/lb; Mining cost: $1.69/t; Sulphide recovery: 91%; Sulphide processing cost: $7.26/t; Oxide (heap) recovery: 60%; Oxide (heap) processing cost: $8.12/t; Oxide (SX-EW) processing cost: $0.30/lb; Concentrate selling costs: $0.41/lb; and Cathodes selling costs: $0.04/lb.

View source version on businesswire.com: https://www.businesswire.com/news/home/20240731222196/en/

Jerrold Annett, SVP, Strategy & Capital Markets

647-273-7351

[email protected]

Daniel Sampieri, Director, Investor Relations & Strategic Analysis

437-788-1767

[email protected]